Are foreclosure rates where they were 15 years ago? Not even close. So why are they not so easy to write off?

By Scott Morgan, Managing Editor

March 18, 2026

South Carolina had the second-highest rate of foreclosure filings in February, according to ATTOM Data Solutions.

It’s a familiar position for the state, which also had one of the country’s highest eviction rates in Q4.

But is that cause for alarm? And what can it really tell us about where we are in the housing conversation as winter draws to a close?

The numbers

In February, ATTOM identified one foreclosure filing for every 3,701 housing units in the United States. In South Carolina, the ratio was one in every 2,217. That’s second only to Indiana, which saw one foreclosure filing for every 1,597 units.

Columbia had the highest foreclosure filing rate among metro areas of 200,000 (but fewer than 1 million), seeing one filing for every 1,433 units –which is more than twice the rate of the country overall.

South Carolina has largely stayed in the top five or six states with the highest rates of foreclosure filings since 2023.

Nationally, foreclosure filings — default notices, scheduled auctions or bank repossessions — are up from a year ago. Compared to last February, the number of foreclosure filings in the U.S. is 20% higher, up to 38,840 units.

But does this mean anything bad? Not necessarily. But also not no.

Supply, affordability, foreclosure, and nuance

South Carolina Realtors CEO Nick Kremydas has called 2026 “the year of the great reset” for the state’s real estate market. With more inventory on the market, there is more availability, and prices have leveled off.

That’s not the same as affordability, of course. Price escalation has slowed over the past three years, yes, spurred in large part to some new supply – 45,510 new construction permits were issued in South Carolina in 2025).

But houses have not really gotten more affordable. The average house price in South Carolina spiked between 2018 and 2023 and has hovered at or near $300,000 since, according to Zillow.

Now, there’s a lot of play in the numbers to get to that average, but a statewide average is a useful metric to show that prices aren’t easing, even if supply issues are.

And the percentage of affordable/attainable/workforce-priced houses is not significantly different than it has been for the past few years. The Homebuilders Association of South Carolina – the industry’s main cheerleader for increasing supply – found in a 2025 study that affordability is out of range for an average of 56% of South Carolinians.

So yes, more houses are coming to market, but meaningful affordable development is still trying to get there.

However, with the return of negotiations and inspections, rather than cash sales and sale prices exceeding asking prices (like they did in 2021), Kremydas says 2026 looks to be a “boring but healthy” real estate market for South Carolina.

To wit, Kremydas has called coverage of South Carolina’s place atop states with the highest foreclosure rates – including my coverage – fake news, saying that framing the state’s housing market in this way is misleading.

“Yes, filings are up,” he says, “and we are seeing a spike in filings in counties like Richland and Dorchester County, but this is not 2008. It’s simply a small pressure relief valve, not a dam breaking.”

Compared to 2008, Kremydas is absolutely right. That year, there were 2.3 million foreclosure filings – 1.84% of homes – in the U.S., according to Pew Research. The annual number peaked at 2.8 million – 2.23% of units nationally – two years later.

In 2025, on the other hand, ATTOM reported 367,460 filings nationwide – representing about one quarter of 1% of U.S. housing units.

This is about where the U.S. real estate market has been since 2022. Foreclosure numbers hit their low in 2020, crept up in 2022, and have mostly stayed steady since.

So no, there’s no reason to panic about the state’s foreclosure numbers in the aggregate.

However, while things are not like they were in 2008, it’s important to understand that things also are not like they were in 2020. Thirty-year mortgage interest rates in 2020 averaged out to 2.65%. Currently, the national average is 6.1%, which is putting pressure on affordability.

The difference in your monthly mortgage payment for the average $300,000 house would be $1,600 vs. $2,000, paying a 2.65% vs. a 6% interest rate and 20% down.

A 2025 report from the National Association of Realtors showed that the share of first-time buyers – 21% – was at an all-time low while the median age of first-time buyers – 40 – was at an all-time high. In other words, fewer Americans are venturing into buying homes, and those who do are waiting longer.

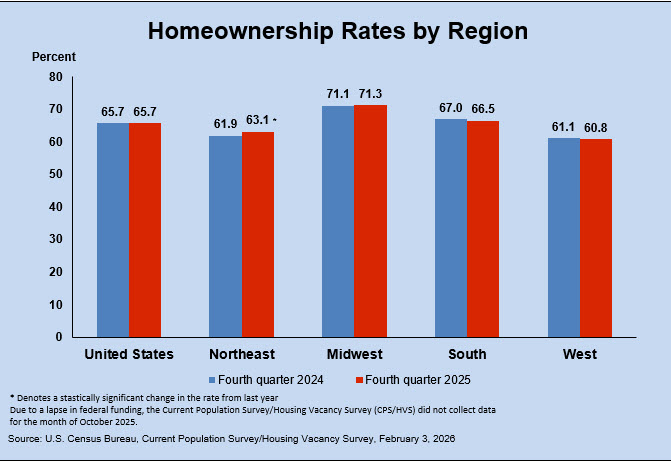

The U.S. Census Bureau reported in February that homeownership rates in the South dipped from 67% to 66.5% from 2024 to 2025 (Q4 to Q4).

So while foreclosure numbers might not be panic worthy, affordability is still an issue.

And pressures could be mounting nationally. According to the New York Fed, mortgage balances grew (by $98 billion) to $13.17 trillion at the end of December, and “the pace of mortgage originations continued increasing, with $524 billion newly originated in the fourth quarter.”

More originations is a good sign, as long as the pace of growth is measured and organic. Too much of a spike in mortgage originations was a major contributor to the collapse of the housing market in 2008.

So …

Even if South Carolina real estate is nicely boring this year, and even if there is no reason to panic right now, it’s not insignificant that the state is out in front of rising foreclosure numbers – even as it’s also out in front of the rate of new houses being built.

Nor is it insignificant that the vast bulk of new housing being built is concentrated in just a few areas of the state, while much of South Carolina – especially rural communities not near growing metro areas – are reaping almost none of the benefits of growth.

South Carolina was the only state to get an A grade for affordability in a Redfin report card last year. Which is nice. But it’s also worth considering that if we’re living in the most affordable state in the country and it’s still so hard for homeowners to make ends meet, 2026 could be a little less boring than hoped for buyers.

{kind=link}

Leave a comment